Atlanta Flexible Office Market at a Glance

#1 Ease of Doing Business

Georgia is the top state for ease of doing business 4 years in a row

Top 7 Searched

Atlanta is the 7th most searched market behind Dallas and Chicago

Millennial Magnet

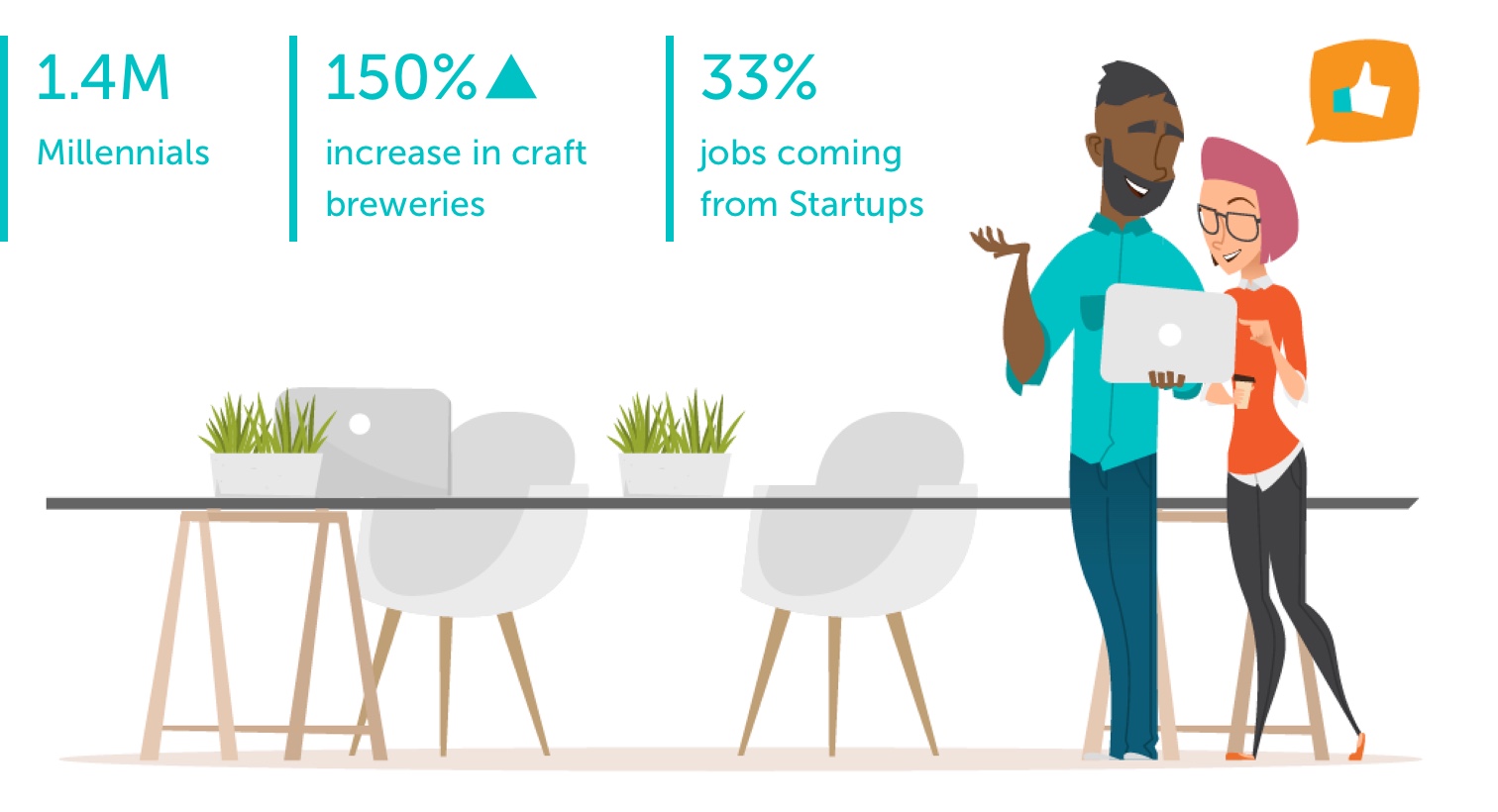

Home to 1.4 Million Millennials

Atlanta is Top 7 for Flexible Workspace Searches

Renting flexible office space is often more affordable than renting traditional office space, especially for the short term. As real estate costs continue to climb in Atlanta for core assets, companies are looking at alternative ways to fulfill their office needs. According to JLL, renters can expect to pay $25.56p.s.f. ▲ for core office space in Atlanta. Rents have steadily climbed for the past 4 years. At 150 square feet per employee, the cost for a core space is about $3,834 per employee, per year. Whereas, the average price per person for flexible office space is $428 / month, adding up to a more affordable $5,139 per year.

Buckhead and Midtown Are Sizzling

Buckhead and Midtown lead as the most expensive, dense and in-demand neighborhoods in Atlanta.

Buckhead is one of the most affluent and beautiful neighborhoods in Atlanta. With business booming, the cost of living in the area also continues to increase. Buckhead is close to Georgia Tech and Georgia State University by public transportation but often proves too expensive for students.

Buckhead boasts over 125 flexible workspaces at an average cost of $2,558 / month.

Midtown is Atlanta’s city center. Bustling with art, cafes and business centers, Midtown is more affordable than other city centers, with average monthly flexible office rent rates of $3,889 / month. There are plenty of options in Midtown, from unfurnished to move-in ready, with amenities that run the gamut. There are 124 spaces in Midtown immediately discoverable and ready to book.

Atlanta Flexible Office Growth Nearly Double

The number of workspaces in Atlanta has seen an 80% YoY increase in venues with flexible office space. This growth comes from strong increases in the footprint and number of spaces from coworking operators as well as building landlords. Both types of space providers have been joining the LiquidSpace platform rapidly in the past year to showcase their space. Today guests can book over 1733 on flexible terms from hours to years. Atlanta’s average monthly cost $2,818 for space is significantly below the national average making Atlanta an affordable market for flexible workspace.

Flexible Office Location Growth in the Last Year

Number of Locations

Core and Flexible Office Trends in Atlanta

Core

Core - stable office space that companies rent out for terms spanning years, mostly for headquarter spaces.

Flexible Office

Flexible - offices rented for spans of hours, months and years for the purpose of satellite space, expansion space, and to provide employees with mobility.

Corporate real estate managers and the C-suite are beginning to build their real estate portfolios to include both core and flexible offices. In fact “65% of enterprise companies plan to incorporate Coworking into their portfolio offering by 2020.” according to CBRE. Core refers to stable office space, which companies lease for terms spanning years. Core office is mostly devoted to headquarter spaces or established markets. Companies rent flexible offices for spans of hours, months and years for the purpose of satellite space, expansion space, and to provide employees with mobility. Flexible offices are often furnished, serviced workspaces – from coworking, serviced office, and direct from buildings.

Atlanta Flexible Office Trends

It’s Easy to do Business in Georgia

Georgia ranks #1 for ease of doing business for four straight years. The ranking takes into account factors from corporate income tax to regulatory environment. Georgia has the highest bond rating from AAA, which makes project funding much more accessible and cost effective than in other states. This access to capital combined with a number-one ranked workforce development program – Quick Start – makes Georgia a prime location for corporate offices. Quick Start has trained over one million employees for close to seven thousand projects. Plus in Georgia there’s solid transportation infrastructure including a top airport hub, which makes Atlanta a no-brainer as a business hub.

Future Focused Millennial Magnet

Atlanta’s relatively affordable, amenity-rich climate is a huge magnet for millennials. Atlanta ranks second after Austin and counts itself as home to 1.4 million millennials. A diverse and educated talent pool is Georgia’s renewable resource. Georgia universities and colleges churn out 300,000 students yearly. No wonder the state witnessed a 150% increase in craft breweries over the last 5 years. All this talent fuels a growing economy with a diverse set of industries and 33% of jobs coming from startups.

Enterprise Coworking on the Rise

Despite rapid development, the 2 million square feet of coworking space in Atlanta still accounts for only 1.5% of the total office stock according to JLL. As the coworking industry matures to accommodate Enterprise needs the trend is favoring larger coworking spaces. According to the CBRE Enterprises Survey “65% of enterprise companies plan to incorporate Coworking into their portfolio offering by 2020”.

The LiquidSpace Q3 Flexible Office Report covers the additional demands that enterprises put on coworking, including culture coding, privacy & security, need for additional amenities, and expansion requirements. Large coworking chains are picking up on this trend. Industrious is expanding its Atlanta footprint to 5 locations compared WeWork’s 4. However, there is still room for independent coworking operators to create a specific culture and fit for the right audience.

I think it started off as one-off situations when businesses had excess space to more thought out office communities (coworking spaces) made up of different businesses. Within that community a deliberate culture is being created and nurtured.

Marguarette Diep

Owner, 3411 Coworking

Top Monthly Spaces in Atlanta

Where do you need space?